Buy Now Pay Later became a thing for retailers, online and in-store. It wads a way to reach shoppers who otherwise may not shop. We all raced to offer it, and promote it.

Humm, Afterpay, Zip and others made it easy, even though the cost to sales was significant, often as high as 6%.

We chased the cult-like BNPL shoppers without a care about what happened down the road.

The trailblazing BNPL companies have plenty of competitors now with PayPal, credit card companies and banks out with competitive offerings. The BNPL road is becoming rocky with consumer organisations and regulators in several countries calling for regulation of the fintech BNPL operators.

With BNPL maturing, there is data as to consumer behaviour, a better understanding as to how the BNPL businesses make money and the role fees, such as late fees, play for consumers who use BNPL.

These and related factors are likely to be behind share price falls for Afterpay:

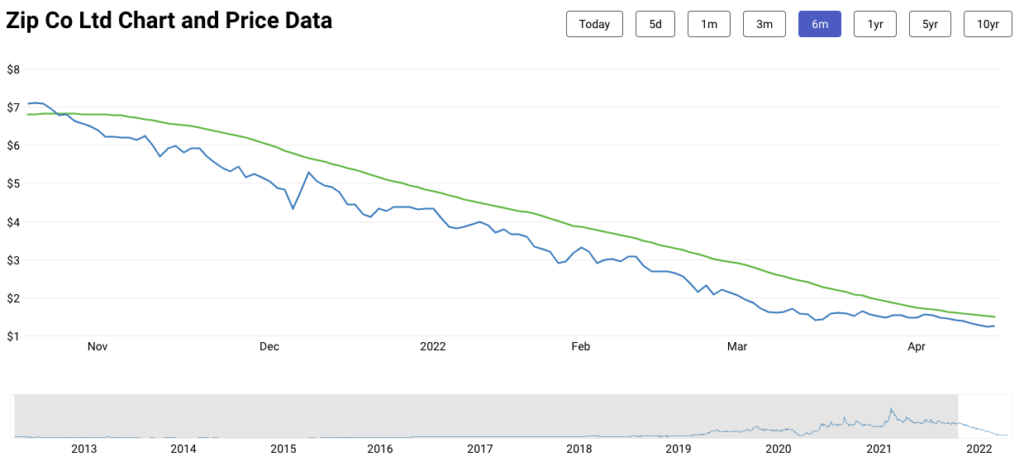

And ZIP:

These charts are from www.fool.com.

Does any of this impact retailers offering BNPL? The increased competition does in that if you want to serve that shopper who relies on these delayed payment terms you are likely to need to expand your offering.

There is commentary that some BNPL businesses are looking at retailers playing a role in responsibility for payment. I am not sure how that could work.

That said, I can understand that their model needs to change, because the current share price trajectory is problematic for them.

Retailers liked BNPL because it did (does?) attract new shoppers and it offered a replacement to LayBy. But the explosion of BNPL is driving issues for the model.

My local coffee shop offers BNPL payment through Payo for a coffee and food. Petrol stations have partnered to offer BNPL for petrol and everyday necessities.

In my own shops I am not a fan of the more extensible BNPL offerings,l like Afterpay. Losing ten percent of margin dollars in a purchase make that purchase less valuable. It’s been a topic at a couple of retailer conferences this year.

While I am no expert, to me it looks like a dramatic increase in BNPL competition, the prospect of regulation and pushback from retailers as to the cost of a BNPL transaction are all impacting the share price, and tarnishing the gloss of the BNPL temple.

I expect there to be a shake out, which is likely to be disruptive for retailers. Eventually, I expect the larger and more traditional financial players to stabilise the BNPL model.

Our job as retailers is to offer what shoppers want, when they want it … and to take payment through any form that works for them and us. So, yeah, just as change is an everyday opportunity in retail, it is thus in terms of how we are paid.

I guess the key point I’d make to retailers about BNPL is be aware of the disruption and be curious and cautious about pitches to take on new payment methods.